50/30/20 Rule Explained

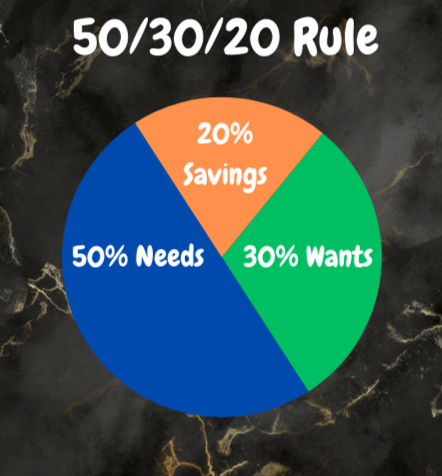

The 50/30/20 rule is a budgeting strategy that splits up your post-tax income into 3 categories: 50% needs, 30% wants, and 20% savings. This method was first introduced by Elizabeth Warren and Amelia Warren Tyagi in their book, “All Your Worth: The Ultimate Lifetime Money Plan” back in 2006.

This straightforward approach to budgeting became popular due to its simplicity. No need to track every penny, no excessive time spent on complicated budgets, and plenty of flexibility to spend on the here and now! Sounds like everyone’s dream right? The trick is to identify each expense and place in the correct category.

Let’s dive into this strategy a little deeper.

50% Needs

“Needs” include the expenses that are essential for survival. In general, think food, water, shelter, transportation here. Of course, most of us will broaden the term “need” to include many other basics. After all, not many of us can get very far without a cell phone! If you made it this far without one, I commend you! But… how exactly did you make it to this blog again?

The point here is to view all expenses and identify which ones we simply cannot do without. After totaling up the cost of these items, it shouldn’t exceed 50% of your take home pay (with the exception of 401k contributions and other deductions). If you happen to be over 50%, one of three things needs to happen. Either it’s time to move some of your “needs” to another column, make an active effort to minimize the cost of certain needs, or just simply make more money. 🤪

Some examples of needs include (but not limited to):

- Rent/Mortgage

- Groceries

- Car Payment

- Insurance

- Utilities

- Minimum Debt Payments

- Basic Cell Phone

- Child Care

30% Wants

“Wants” are all the expenses that aren’t critical to your survival. That’s right, we’re talking about the fun stuff! Things like tickets to a show, vacations, and restaurants all belong here. Don’t trick yourself into believing that a want is actually a need. That massage probably felt great after your workout, but would you say it was actually essential for your survival? Moreover, is that monthly gym membership actually a need if you can exercise for free?

This category also includes expenses incurred from choosing to upgrade from an actual need. For example, I’ll be the first to admit you need a cell phone, but do you need the absolute latest and greatest cell phone? No, I’m not insinuating you should have a flip phone, but deciding on a phone that’s a few models older will fit the needs of most people.

Some examples of wants include (but not limited to):

- Live Events

- Restaurants

- Travel/Vacations

- Extravagant Clothing/Accessories

- Subscriptions (Amazon, Netflix, etc.)

- Memberships (Gym, Bowling League, etc.)

- The Latest Tech

20% Savings

“Savings” will include all the hard-earned money being put towards your great, big, beautiful tomorrow! In general, this includes income being directed towards emergency savings, retirement, down payment for future purchase of property, or even any extra payments put towards debt.

We have discussed some of the best tactics to a Savvy Solo can approach savings in the past. 6-9 months of emergency savings is preferred, there’s the Bucket Fund Strat, prioritizing high interest debt payoffs, etc. The 50/30/20 Rule kind of lumps it all together into one category without clear direction totaling 20% of your take-home income. Still, a savings rate at 20% would greatly surpass the American averages, so (if nothing else) it’s a great goal to shoot for in the beginning.

Some examples of savings include (but not limited to):

- Retirement Savings (401k, Roth IRA, etc.)

- Emergency Fund

- Extra Debt Payments

- Down Payment for Property

- Short-Term Savings Goals

50/30/20 Rule in Action!

Let’s say that Savvy Solo Susan makes $6k per month after taxes. Way to go Susan, you are killing it! She would want to allocate $3,000 per month towards needs, $1,800 towards wants, and $1,200 towards savings. We mentioned that Susan is indeed quite savvy, so she has everything mapped out on the MFC!

Susan doesn’t have any high interest debt going on and has figured out a number of ways to decrease her fixed costs. In fact, looks like she has been allocating a total of $2,500 per month between her available retirement vehicles and emergency fund, which puts her savings rate at north of 40%, hooray! According to this method, Susan has the ability to reallocate $1,300 per month towards needs and wants if she so chooses!

Alright, now let’s take a look at the other side of the spectrum with not so Savvy Solo Nick. Nick is making the same income as Susan but unfortunately got himself into credit card debt over the last few years. His total necessities (including rent, minimum credit card payments, etc.) come to $3k per month which falls right in line with 50% towards needs.

Following the 50/30/20 Rule, Nick decides to forego his 401k company match and allocate $1,200 towards extra credit card payments. With his 30% allocated towards wants, Nick spends $1,800 over the course of the month on going to the movies, baseball games with friends, and a nice watch he’s had his eye on. Technically, Nick is following this rule exactly as it’s laid out. That said, just about anyone in the world of personal finance would say that this is a horrible plan! What are you doing Nick?!?

Pros & Cons

The 50/30/20 Rule can assist a lot of people who are just getting started on their personal finance journey. It provides straightforward guidelines that are relatively easy to measure. Being forced to determine if each expense is a want or a need is absolutely essential towards building future wealth.

That said, there are a few aspects of this budgeting approach that don’t jive. I don’t love the idea of setting a blanket % of each category across the board. There are going to be periods of life, sometimes years at a time, that a solo has legitimate needs greater than 50% of their after-tax income, and that’s ok! It’s all about utilizing the resources you have to make your life better now and for the long run.

I also don’t like the idea of extra payments towards debt being counted towards “savings.” In the above example, Nick is technically putting 20% of his income towards “savings.” Unfortunately, he’s neglecting retirement and emergency savings, while also spending unnecessarily. If this continues, it could put him in hot water in the future. He would be better off utilizing something like a 45/10/45 Rule for a time till he got himself on better footing.

One of the problems with blanket budget plans in general is that they won’t prioritize the goals of the individual. If a young Savvy Solo is looking to FIRE, they might look to aim for a 30/10/60 Rule. If a divorcee with 3 kids, high expenses, and a job they enjoy is looking to get their financial house in order, a Savvy Solo might be perfectly suited by shooting for a 70/15/15 Rule. One size does not fit all, it’s all about bringing the most value to your specific situation.

Pros:

- Straightforward framework

- Simple outline for beginners

- Helps identify needs vs wants

- Prioritizes needs over wants

- Promotes tracking spending and categorizing expenses

- Easier to maintain vs a zero-based budget

- 20% savings goal is higher than the national average

Cons:

- Prioritizes wants over savings

- Extra debt payments counted towards savings

- One size fits all approach

- Difficult to manage with irregular income

- Gray area on wants vs. needs

- People currently at 20% savings rate not motivated to do more

In Conclusion

If you happen to be new to budgeting, the 50/30/20 Rule is a great way to get started. It helps prioritize some level of saving for the future and differentiate between wants and needs. If you have never tracked your spending before, this process can be quite eye opening. Also, since I’m not a fan of tracking every cent, this strategy is relatively simple to maintain once you get going.

Instead of this method, I would argue that coming up with a savings strategy that is value driven (instead of needs vs wants) will naturally stick around longer. The strategy that I implemented involves looking over each expense and evaluating if the cost is worth the value that I am getting out of it. Sure, we all need a cell phone, but with the 50/30/20 Rule it may be difficult to determine if the iPhone 16 Pro Max is considered a want or a need.

In general, doing something is better than doing nothing. If the 50/30/20 Rule is going to get you motivated to make changes, then do it! Getting in the habit of budgeting will lead to true wealth and, in turn, more time spent doing the things that you love!

Stay classy Solos! ✌️