What is it?

Your credit score, which is commonly referencing your FICO score, is based off information in your credit report. The FICO score is not the only type of credit score, but it is considered the industry standard and is used by the vast majority of lenders to determine risk. Generally speaking, the FICO score is the one you’ll want to track to gage your current standing. It’s calculated using the 5 categories referenced above, and ranges from 300 to 850 (the higher the better).

Unfortunately, FICO does not give us a precise formula as to how each individual score is created. Different events could have different impacts on different people, which makes it a bit challenging. For instance, someone with short credit history making one late payment will be more heavily impacted than someone with a long credit history. Since the credit report (and thus the credit score) alter frequently and are dependent on so many factors, there is no exact equation on how a particular event could impact your unique credit score.

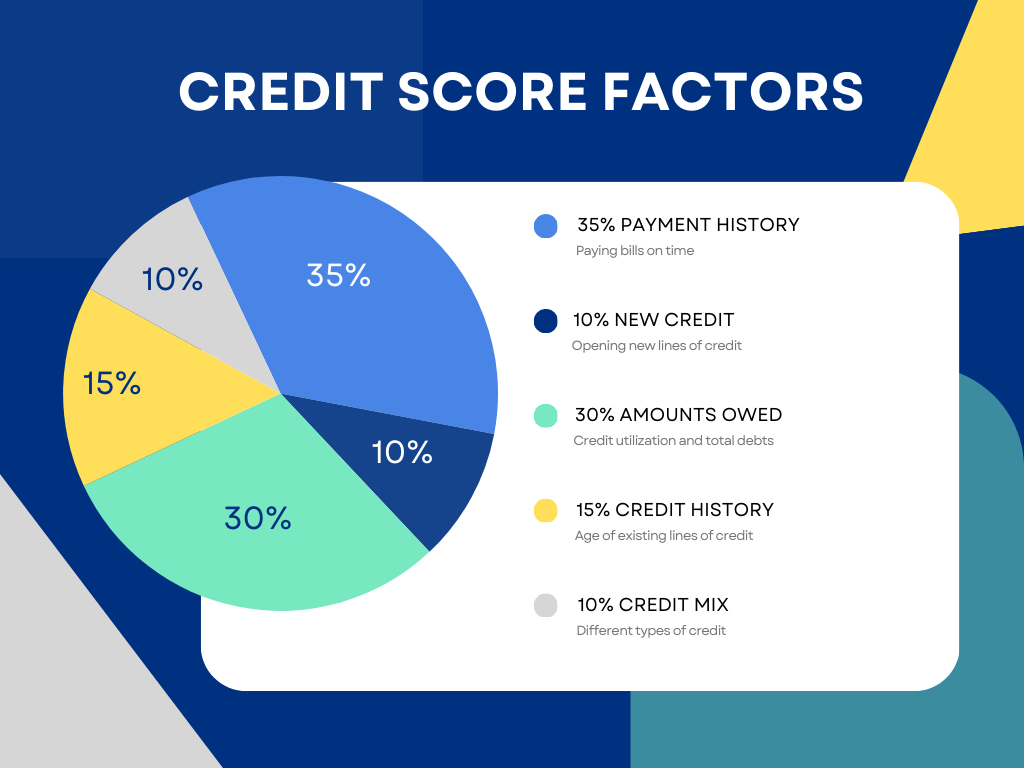

FICO has, however, provided a guideline on what categories weigh the most on your score. While the calculation of your credit score may not be an exact science, it’s important to know what areas to focus on when looking to improve it. Let’s explore these different factors.

35% Payment History

The biggest impact on your credit score is your history of paying bills on time consistently. Back when we discussed the best practices on credit card use, I had made an extreme emphasis on paying your bills on time. Other than racking up extra fees and interest, missed payments will be the heaviest weight on your credit score. According to this article, by Beverly Harzog, even a single reported missed payment could be a black mark on your credit report for years to come.

“Even after you pay the past-due bill, it remains on your report for around seven years starting from the original date of delinquency.”

Seven years!!!!! Many late payments aren’t reported to the credit bureaus if paid within 30 days of the original due date but there is no guarantee of that. Also, the longer you wait to pay it (going from 30 to 60 to 90 days) will cumulatively impact your score as time goes on. 😬

Obviously paying timely on things like credit cards, student loans, and mortgages are going to have a positive impact here. But also, non-debt dues like the electric bill, cell phone bill, and car insurance payments could be a factor. Any of these companies have the potential of reporting a late payment to the credit bureaus, which would then go on your credit report, thus resulting in a diminished credit score.

Not all events in payment history are created equal. A bankruptcy is obviously going to have a much larger impact than a couple of small late payments that were cleared up quickly with a cell phone carrier. One key point here is to make a deliberate effort to make all minimum payments in order to avoid 3rd party collection agencies if possible.

The more accounts tied to your name with consistent on-time payments will have a fantastic impact on your credit score. Payment history is the biggest factor in your credit score, this area should be given the most amount of attention.

30% Amounts Owed

The next biggest chunk of the pie is total amounts owed. This area looks at your total debts and your credit utilization rate. It’s worth noting that the amount of debt you currently hold is not nearly as significant as your credit utilization. Essentially when someone uses a high percentage of available credit, this can be a red flag to a lender that this person is overextended.

When looking at your credit report for this area, FICO is looking at the following:

- Total amounts owed

- Amounts owed on different types of accounts

- % of accounts carrying a balance

- % still owed on installment accounts (mortgage, student loans, etc.)

- % of credit utilization on revolving accounts (credit cards, HELOC, etc.)

The first 4 items don’t have as large an impact as the last one. When it comes to installment loans, for example a car loan or a mortgage, paying extra on the total debts a little extra each month will tend to have a slight positive impact. Far more important is to pay the minimums on time to these accounts, or it would have a big negative impact on your payment history (above).

When it comes to this category, it’s important to focus on your credit utilization rate. Again, back to when we discussed credit card use, I had emphasized the importance of keeping your credit utilization below 30%. Going over 30% will negative impact, consistently keeping it under 10% will have a positive impact.

In simple numbers, let’s pretend you have one credit card with a credit limit of $10,000. Throughout the month you make a bunch of purchases on this card totaling $5,000 completely prepared to pay this amount in full before the due date. The credit card company reports to the credit bureaus that you have a current balance of $5,000 (not necessarily a late balance, mind you). Your credit utilization rate right now is 50% and will negatively impact your credit score.

Keep in mind this negative impact is temporary and will come back relatively quickly with healthier credit use practices moving forward. Credit card companies typically report the balance of the credit card on its closing date, which is usually different from the due date. To avoid overthinking all this, the Savvy Solo would usually want to have credit lines totaling 10X their average monthly credit usage.

15% Credit History

One’s credit history refers to the length of time an individual has had access to credit, and the average age of all credit accounts. Essentially, the longer you have had credit lines open in good standing, the better your credit score is impacted. Having a long history of on time payments helps lower your risk level to lenders.

When considering credit history, here is what they are looking at:

- Time since first credit line was established

- Age of current oldest credit account

- Age of newest credit account

- Average age of all standing credit accounts

Other factors of your credit score are concentrated on how well you are managing your debt and/or lines of credit, this area primarily focuses on how long you have been doing it. This does not mean that someone with a short credit history can’t have a great credit score; but it could mean that credit events for this person get magnified. To maintain a high credit score early on in your credit journey, it’s imperative to pay bills on time and keep credit utilization to a minimum.

Of course, the big joke here is that you can’t get a solid line of credit without a long credit history, and you can’t get credit history without a line of credit. We’ll get more in depth on best practices to achieve and maintain a good credit score, but for now it’s best to start small and work your way up. This area can only be improved with healthy credit practices over a longer period of time, and only consists of 15% of your overall score.

10% New Credit

One’s credit report is going to classify credit lines established in the last two years as “new credit.” This area will also reflect the number of recent inquiries you have (also detailed in one’s credit report for two years). FICO states that it only considers inquiries and new accounts made in the last 12 months when factoring this area of one’s FICO score.

Essentially, a rash of new inquiries and credit lines in a short period of time (particularly for one without a long steady credit history), is going to raise red flags for lenders. It could mean the individual has experienced a life event that makes them higher risk to lend to.

Here are some factors that impact this space:

- Age of newest account

- Number of new accounts

- Number of recent inquiries

The number of inquiries on your account will have less of an impact than the number of new accounts. Also, it’s worth noting that there are “hard inquiries” that occur when lenders check your credit with the purpose of installing a new line of credit or loan, and “soft inquiries” that occur when your credit score/history is checked without this intention. Soft inquiries do not appear on your credit report, therefore, do not impact your credit score.

People with a long healthy credit history might see a small temporary ding in their credit when applying for a new loan or line of credit, while people with a short credit history might see a larger impact especially if applying for multiple lines of credit in a short period of time. Keep in mind that new credit only accounts for 10% of your credit score and shouldn’t impede the Savvy Solo from making the big picture moves to better their situation.

10% Credit Mix

When looking at the credit mix, lenders are looking for one’s experience of managing different types of accounts. Basically, they like to see that you have been steady at handling different kinds of credit lines over a period of time. These various types of credit generally fall under two categories: revolving credit and installment credit. They might include the following:

Revolving Credit:

- Credit Cards

- HELOCs (home equity lines of credit)

- Retail store cards

- Business lines of credit

Installment Credit:

- Mortgages

- Car loans

- Student Loans

- Personal loans

Essentially, lenders like to see that you are experienced in managing different types of loans and/or lines of credit. Does this mean you should go out and start applying for types of credit you don’t need to utilize? Absolutely not! If you happen to have a mortgage and a couple of credit cards, there’s no need to explore HELOCs in an effort to improve this area.

Credit mix only has a 10% impact on your overall score, don’t let it get you into trouble with unnecessary lines of credit. Furthermore, don’t let this impede you from paying off certain loans. If your only current installment credit is a car loan, paying it off might have a temporary ding to your credit score, but will prove to give you the better overall score in the long run. Don’t forget, this car loan (even after paid off), will positively impact your credit history, amounts owed, and payment history.

Considering The Score

When looking at your credit score, lenders consider it a snapshot of your ability to manage debt/lines of credit in the past. Your individual credit score may change each month, it’s important to not get hung up on small changes (either up or down) when evaluating. Instead, we are looking to utilize this number as motivation to improve and maintain a healthy credit score for the long term.

What’s a good credit score? As we established, a credit score can fall anywhere in between 300-850. FICO established the following ranges:

- 800-850: Exceptional

- 740-799: Very Good

- 670-739: Good

- 580-669: Fair

- 300-579: Poor

Generally speaking, anyone with a credit score of 780 or above will have access to the absolute best available interest rates and get the golden star of approval from the majority of lenders. Even those in the 700-770(ish) range will get excellent rates, possibly a fraction of a percent less than those in the exceptional range. Use your current score as motivation to continue making smart decisions and to build on your financial future!

Conclusion

I love to gamify everything. It helps motivate me to play the game and keep things fun while seeing real life improvements in areas of my life. That being said, most people should not be targeting to achieve (and especially maintain) a perfect 850 credit score. There are a million factors at play with determining your credit score on an ongoing basis, many of which might be out of your control. It’s my experience that setting an unrealistic goal leads to disappointment, which can result in a lesser overall performance in many cases. Don’t forget, 780 or better is really all you need to be at the top of the mountain; and over 700 will get you what you are looking for most of the time anyway.

Different factors that make up the credit score tend to work against each other. For example, you may be looking for a new credit card to support your credit utilization rate, but that might ding your new credit and credit history factors. In this case, the Savvy Solo would still get the credit card since credit utilization has a much larger impact on the score overall. Don’t get caught up in what might temporarily ding this number, instead focus on what will have the bigger impact over a long period of time.

I’m hoping this post shed some light on to how your credit score is calculated. Someone in my life gets very hung up on 3-point swings up or down, don’t be that guy. Unless you are in the NBA, 3s aren’t going to make or break you 🤪. In a future post we’ll discuss best practices when looking to improve the credit score, and how it can impact your daily life, for better or worse.

Stay classy Solos! ✌️